The AI Business Through a Crypto Miner's Eyes

In the last piece, NVIDIA Through a Crypto Miner’s Eyes, I looked at NVIDIA through the lens of my mining years and saw two things. One was its fragility: value is shifting from training to inference, from general-purpose chips to custom silicon, and the segment NVIDIA is counting on most is exactly the one being hollowed out from within — while the company itself has started investing in its own customers, adding leverage to its own demand. The other was more fundamental: even if NVIDIA is the hardest pick-and-shovel play of this AI wave, that doesn’t prove today’s price is rational. Whether a technology is real and whether its stock price makes sense are two different lines on two different charts.

This time I want to look higher up the stack — not just NVIDIA, but the entire AI industry.

The AI business is red-hot right now. The four major tech giants’ combined capital expenditure for 2026 tops $700 billion, up roughly 80% from last year. Bonds, venture rounds, and stock prices are all riding the same wave. The business is “running” — people are paying, the ChatGPTs of the world have real subscription revenue. But revenue is just revenue. I want to ask a simpler question: when does this business actually turn a profit? Meaning: out of all that money pouring in, is there any layer in this stack that can earn enough from end users to sustain itself, justify today’s valuations — and not just create the appearance of prosperity through round after round of investment?

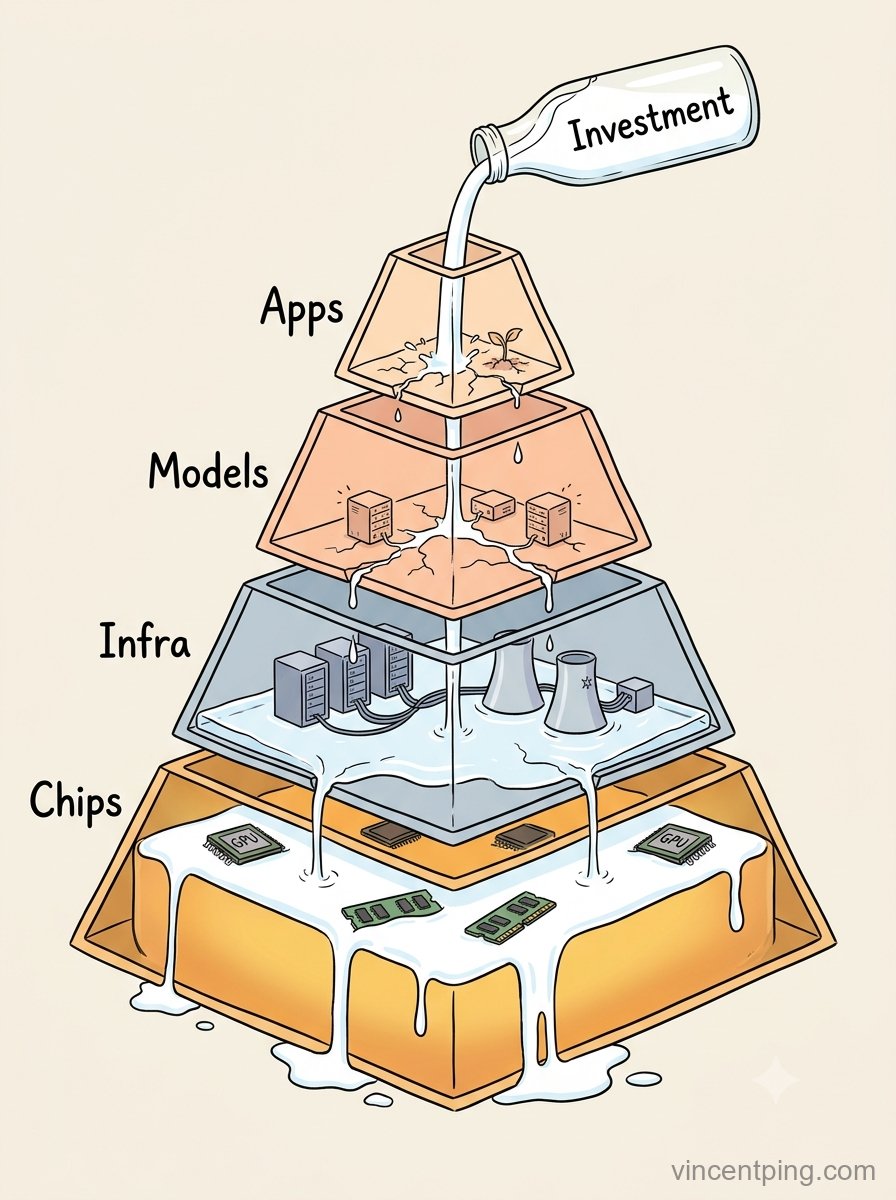

The Base of the Pyramid: Chips

To see where the money actually lands, start with an honest admission: someone in this chain is making real money — right at the bottom, in the chip layer.

NVIDIA, TSMC, and the high-bandwidth memory suppliers like SK Hynix — these are the people genuinely cashing in. Their shared advantage is simple: regardless of whether infrastructure, models, or applications above them ever turn a profit, as long as this arms race keeps going, everyone has to buy their chips, their fab capacity, their memory. The chip layer is the one tier that’s reliably profitable today. NVIDIA’s gross margins are absurdly high. The HBM memory suppliers are minting money on tight supply.

But notice two things.

First, this windfall isn’t as stable as it looks. On the NVIDIA side, I covered this in the last piece: inference — the segment NVIDIA has the biggest hopes for — is being eaten from the inside by custom chips. The bar for building an inference-specific chip isn’t that high, so the largest buyers are designing their own, and new entrants keep piling in. This territory will be hard to monopolize.

On the memory side, it’s a different kind of instability. Memory is a notoriously cyclical industry. The script repeats every few years: supply gets tight, prices spike, capacity floods in, prices crash 50%, margins go negative. It’s played out this way for three decades.

Here’s the interesting part. This round, as memory makers rake in record profits, they’re all saying the same thing: this time is different — AI demand is structural, it has “ended the cycle,” and prices can stay elevated indefinitely. But every time a bubble nears its peak, the loudest chorus is always “this time is different.” Cisco was justified at more than 200x earnings with the same line: “the old rules don’t apply anymore.” An industry that has convinced itself the cycle has been abolished is usually standing right on top of one.

So the memory windfall, as I see it, is riding the cycle — not transcending it. When it turns is hard to say, but the louder “this time is different” gets, the closer the turn usually is.

The second point matters more: the chip layer’s profits don’t appear out of thin air. They’re extracted from the layers above — infrastructure buys its GPUs, models pay infrastructure rent, applications foot the bill for all of it. The harder chips squeeze, the tighter every layer above gets squeezed.

In other words, the chip layer’s profit is everyone else’s cost. So “someone is making money” doesn’t refute “this business isn’t really making money yet” — it is the problem. All the money sinks to the very bottom, and the higher you go — the closer you get to where value is supposed to originate — the worse things look. And don’t forget: trace the chip layer’s revenue all the way up, and most of it isn’t coming from end users willingly paying for an AI product. It’s coming from the tech giants’ own reserves, their venture rounds, their debt — money they’re pouring into the arms race. The one layer that’s reliably profitable is profiting from investment, not revenue.

Infrastructure: A Hole Waiting to Be Fed

One layer up from chips sits infrastructure — compute, data centers. Wall Street’s dominant narrative right now is “sell picks and shovels at the gold mine”: nobody knows which model wins, but everyone needs compute, so investing in infrastructure is a sure thing.

Infrastructure is actually the most worrying layer of all.

I mentioned in the last piece that a mining rig is a cash-burning heavy asset — power bills, depreciation, maintenance, every single day. An AI data center is the same thing, only heavier. It has to buy the most expensive GPUs from the layer below — cards that get outclassed by the next generation in two or three years and get their lifespan cut short by 24/7 full-throttle operation. Then it has to keep buying electricity. Compute’s endgame is power. Every training run and every inference call burns watts. The big players are signing multi-decade, multi-billion-dollar power purchase agreements just to lock in stable supply. GPUs, power, cooling, maintenance — all cash out the door. The GPU bill flows down to the chip layer and becomes its monopoly profit. The rest — power, cooling, maintenance — is operating cost that vanishes the moment it’s spent. Bleeding from both ends.

And infrastructure isn’t the destination. It produces compute, but someone has to use that compute and actually make money from it before infrastructure can break even. Whether it recoups its investment depends entirely on whether the models and applications running on top of it can earn enough to feed it. The problem is right here: the money feeding infrastructure today is still mostly investment from above, not revenue earned from end users.

How hungry is this hole? One number tells the story. Alphabet, Google’s parent company, had over $73 billion in free cash flow in 2025. According to analyst projections, AI infrastructure spending will drain that to roughly $8 billion in 2026. Most of the money went to buying GPUs, feeding this layer. Alphabet even started issuing bonds to fill the gap — a company that prints cash like a mint, forced to borrow because infrastructure is sucking it dry.

And even the profits that show up on infrastructure’s books are inflated. These GPUs become obsolete in two or three years, but they’re often depreciated over five or six on the balance sheet — the gap quietly turns into better-looking profits on the income statement. This isn’t speculation: over the past two years, the major tech companies have been quietly stretching the depreciation schedules for AI chips to five or six years. Did the actual useful life of the hardware change? No. But the reported profits got a boost anyway. Even Michael Burry — “The Big Short” — has publicly questioned this practice: using extended depreciation to make profits look better than they are. In other words, infrastructure isn’t just bleeding cash constantly — even the presentable numbers on its financial statements are dressed up by accounting choices.

Models and Applications: A Layer That Hasn’t Split Yet

One more layer up, we get to the large language models running on all that compute. Will this be the layer that makes sustainable money? Intuitively, it should be — this entire AI breakthrough is a breakthrough in large models.

As things stand, large models will have a hard time earning monopoly profits.

One reason is competition from Chinese models and the progress of open source. Companies like DeepSeek are producing near-frontier performance at a fraction of the cost — and open-sourcing it. Open-source models keep closing the gap on closed ones. You’re ahead this month; open source catches up by next month, and the distance keeps shrinking. When something of comparable quality is available for free, the logic of “my technology is superior, so I can charge a premium” stops working.

Models have another trait: user loyalty is extremely low. Whichever one works better this month gets the traffic. Switching costs are essentially zero. This is nothing like Facebook or social networks — you can’t leave those because everyone you know is on them. Models aren’t sticky. People use whichever is best and jump without a second thought. Anthropic briefly overtaking OpenAI is a case in point.

Look more closely and you find that the model layer isn’t just “not profitable” — it’s bleeding money at scale. Take OpenAI, the front-runner: annualized revenue for 2026 is somewhere north of $20 billion, which sounds impressive, until you see the projected $14 billion loss in the same year. For every dollar coming in, roughly 70 cents is going out the other side. Out of hundreds of millions of users, only a small fraction pay. Over 90% use it for free — and every free API call’s compute cost comes out of OpenAI’s pocket. The hole gets filled by round after round of fundraising. So the model layer works the same way as infrastructure: the money it burns is overwhelmingly investor capital, not revenue earned from end users. What it brings in from customers doesn’t cover the cost.

What about applications? At the very top of the pyramid, there should be a layer where apps make money. But try to isolate that layer today and you’ll find it barely exists. The most usable applications — ChatGPT, Claude — are built by the model companies themselves. Models and applications haven’t separated yet. Beyond those, a wave of smaller players are building image generators, voice tools, video tools — but they’re either burning cash training their own models or relying on the big players’ APIs, and they can’t get costs down. The market looks busy on the surface, but it’s miles from ordinary people’s daily lives. Most people play with it and move on. Watch the media cycle: one model drops a new version, a crowd rushes over to test it; next week another company ships a new feature, and the crowd rushes over there. Any stickiness at all? No must-have use case, no moat, all of them surviving on transfusions.

Truly independent third-party applications — ones not tethered to a big-model company — are still rare. That’s a sign the market is just getting started, nowhere near mature. A revolutionary technology breakthrough, without broad creative participation from society at large, relying on a handful of model companies tinkering by themselves — that’s not how killer apps get born.

The Assumption That Got Priced In as Fact

Connect all these layers and something interesting emerges.

The staggering valuations across the AI industry today — triple-digit P/E ratios, market caps that have priced in years of future expectations — all of them rest on a single assumption: this business will eventually earn long-term, sustainable, monopoly-level profits. Only monopoly profits can justify multiples like these.

But walk through the pyramid layer by layer. The only tier actually earning monopoly profits is chips, at the very bottom — and those profits are extracted from every layer above, while the monopoly itself is likely to be eroded by custom inference chips. One layer up, infrastructure is a hole waiting to be fed. Above that, models can’t hold a monopoly and are hemorrhaging cash. And the topmost layer, where applications are supposed to make money? It hasn’t even emerged yet.

The assumption underpinning every sky-high valuation — “this will produce long-term monopoly profits” — fails at every link. Each one is either already broken or far from proven.

Here’s a simple way to sum up the present: the market has priced in something that is far from certain, as though it were already certain.

Google makes a good illustration. Google designs its own TPUs, builds its own data centers, runs Gemini, and stuffs AI into Search and every product it has — it’s a miniature of the entire AI supply chain in one company. Can that AI supply chain feed itself? No. It still survives on the cash its old search-advertising business earns every day, constantly transfusing it into the new one.

What does that tell you? After all this money poured in, even Google hasn’t grown a single new, self-sustaining, must-have application out of AI. What about everyone else?

The truth is, for this AI business to become self-sustaining at this stage, what’s missing isn’t just money. What’s most missing is time.

For the AI industry to stand on its own, it needs the creative energy of society at large — widespread experimentation, from which a generation of killer apps can emerge and grow into genuine necessities, the kind people truly can’t live without. Only then can we say AI is a business with a future. Until that happens, AI is an infant that needs to be fed constantly.

Growth takes time. Time to bring down the cost of the technology. Time to educate and onboard the public. Time for applications to seep into daily life and habits. You can’t rush it.

But time is the one thing capital has the hardest time giving. Money can be deployed all at once. It can’t sit patiently while something grows for years.

References

- Sequoia Capital, David Cahn, “AI’s $600B Question” (sustaining current capex requires ~$600B in annual revenue; December 2025 update notes end-user revenue still “tens of billions per year” while infrastructure investment is “trillions over the next five years”): https://www.sequoiacap.com/article/ais-600b-question/

- CNBC: Major cloud companies’ combined 2026 capex ~$700B; Alphabet’s free cash flow projected to plunge ~90% from $73.3B (2025) to ~$8.2B; multiple bond issuances, long-term debt quadrupled in one year to $46.5B (Pivotal Research et al.): https://www.cnbc.com/2026/02/06/google-microsoft-meta-amazon-ai-cash.html

- CoinDesk: Public Bitcoin miners pivoting en masse to AI data centers, $70B+ in AI/HPC contracts signed, AI projected to account for ~70% of their revenue by end of 2026: https://www.coindesk.com/markets/2026/03/27/bitcoin-miners-are-becoming-ai-companies-and-selling-their-btc-to-fund-the-transition

- On cloud companies extending server/GPU depreciation from 3–4 years to 5–6 years, inflating reported profits (including Michael Burry’s criticism): https://www.cnbc.com/2025/11/14/ai-gpu-depreciation-coreweave-nvidia-michael-burry.html

- Goldman Sachs on AI infrastructure spending scale and GPU depreciation schedules (“industry commonly depreciating over 4–6 years, mismatched with NVIDIA’s annual upgrade cadence”): https://www.goldmansachs.com/insights/articles/tracking-trillions-the-assumptions-shaping-scale-of-the-ai-build-out

- On Google TPU, Amazon Trainium/Inferentia, Microsoft Maia, Meta MTIA and custom inference chips eroding general-purpose GPU market share: https://www.stanleylaman.com/signals-and-noise/gpus-how-long-do-they-really-last

- CNBC: Memory industry’s cyclical boom-bust history (Micron et al. — prices halved, margins turning negative, stocks dropping 50–60%), current “AI has ended the memory cycle” optimism, and peak-risk indicators; top three manufacturers control ~95% of global DRAM capacity: https://www.cnbc.com/2026/05/25/memory-stocks-cyclical-boom-bust-samsung-sk-hynix.html

This article was written in June 2026. All figures are publicly available estimates as of that date; sources and methodologies vary, and numbers will change over time. Please verify against the latest primary disclosures before citing. This is personal observation and analysis, not investment advice.

Subscribe by email

Get new posts delivered straight to your inbox.

Your email is only used for new-post notifications. Unsubscribe anytime.